TYPES OF STORE

v Generally

unworked material is known as store and the place where it is housed called

“Store Room”.

v Stores

are generally of the following categories:

(a) Raw

materials.

(b) Consumable

stores.

(c) Inflammable

stores like petrol, kerosene oil etc.

(d) Chemicals

like carbide, sulphuric acid etc.

(e) Machinery

and Equipment.

(f) Hand

Tools.

(g) Furniture.

(h) Finished

Products.

(i) Scrap.

(j) Unserviceable

stores.

(k) Empties

and Packages etc.

v Finished

product ready for sale are called stock and the place where they are kept

called “Stock Room”.

ORGANISATION OF

STORE AND PURCHASE DEPARTMENT

v In small factories or concerns, the store room and stock room may be one and under the control of one officer but in big organisation both are separate and are separately controlled.

v The organisation of the store department is as follows:

v The

store-keeper is very important figure in any organisation and he is as much

responsible for the articles in his charge as cashier for the cash.

v He

should, therefore, take steps to reduce thefts and wastage of materials to a

minimum.

PURPOSE OF STORE

KEEPING

v To

see that the stock of no item at any time falls below the prescribed minimum or

goes in excess of fixed maximum quantity.

v To

examine carefully all goods and materials on receipt.

v To

arrange for a systematic and efficient storing of materials.

v To

maintain accurate and prompt distribution of items to departments as and when

required under Issue Requisition Notes.

v To

maintain efficient quantity records of movement of stock and to account for all

goods that has come under their charge.

v To

prevent any theft, wastage or deterioration of stock.

DUTIES OF STORE KEEPER

v The

first most important duty is to plan the stores. He has some space at his

disposal and has to put that space to the maximum use.

v To

keep record of materials and their costs.

v Whenever

requisition are received from shops, they are checked and if found correct,

material is issued and entries are made in the required register.

v He

has to check the balance of items from time to time and see that desired

quantities are available.

v Whenever

the existing stock at any time is likely to be exhausted he should send its

information to store officer, who in turn will inform to purchase section.

v He

has to prevent leakage, theft, wastage and deterioration.

v He

has to see that material is issued only against written requisition.

v He should not permit everybody to go inside and issued materials must be handed over outside the store, so as to prevent theft and disturbances.

IMPORTANCE

OF RECORDS AND REGISTERS IN STORE

v Mostly

stores accounts are referred to the details pertaining to the material which is

not for resale.

v A

better stores procedure is a safeguard against waste of material and theft etc.

v In

order to maintain an efficient record of stores, the following books and

records will be required and these are maintained separately for different

types of materials:

(a) Inward

and Outward Registers:- When the material is despatched by the supplier through

rail, he will send its receipt issued by the railway authority, called ‘RR’.

ð On

the production of that receipt to railways, material can be received by the

customer.

ð A

separate register is maintained by the store-keeper in which daily entries of

RR received are made and known as “Inward Register”.

ð In

the same way, when some material goes out of the store to other place, its

entries of RR are made by store-keeper in “Outward Register”.

(b) Stock

Register:- These are:

(1) Dead

stock or Non consumable Register:- This is maintained by store-keeper, in which

entries of non-consumable articles such as machinery, furniture etc. are made.

The different items are entered in different pages. All transactions about a

particular item are entered in one page.

(2) Consumable

Register:- In this, store-keeper maintains record of consumable stores

received, such as coke, diesel oil, lubricants, cotton waste, paints etc. The

different items are entered in different pages. All transactions about a

particular item are entered in one page.

(c) Daily

Receipt Register:- This may be in a register or loose leaf from.

ð Whenever

any material comes in the store, it is entered date wise in daily receipt

register.

ð Material

is then inspected ad if found suitable is entered in Stock Register.

ð If

the material is found defective, it will be rejected and either the material or

its reports will be sent to the supplier.

ð The

incidental charges that are incurred will also be noted in daily receipt

register.

(d) Issue

Register:- This may be in register or loos leaf form. All stores issued are

entered date wise in it by store-keeper. From the receipt and issue register,

store ledger is prepared by accounts section.

(e) Surplus

Stock Register:- Sometimes such purchases are made, which do not come in use

for long time, say (3 years).

ð Such

materials are then declared surplus and are recorded in a separate register

called Surplus stock Register.

ð Thus

unnecessary material is removed from the stock register to facilitate easy

handling.

(f) Suspense

Register:- The defective items received in excess should not be placed in the

bins but in “Suspense cell”. A separate register is maintained by store-keeper

for all such items placed in suspense and is known as Suspense Register.

(g) Condemned

Article Register:- Unserviceable material after use or obsolete material which

is authorised to be condemned by authorised persons is entered in this register

and will be shown as stock until disposed off some way.

ð The

balance of condemned article will be taken out from store ledger and will be

shown condemned.

(h) Loan

Register:- Sometimes non-consumable material is issued from store on loan for

temporary period by the production of slip of authority.

ð Before

issuing, material is entered in this register and signature of the bearer is

taken in this register and slip of authority is kept safe.

ð When

the material comes back, slip is returned and entry of material received back

is made in loan register.

(i) Empty

containers and Packages Register:- The record of empty containers and packages

is kept in this register by store keeper.

ð These

should be disposed of at convenient intervals by auction or otherwise the best

of advantage.

ð The above are the various records which must be kept by any store-keeper for easy and smooth handling of stores.

ADVANTAGES

OF GOOD STORE RECORDING SYSTEM

v Ready

record of all materials and stores purchases may be obtained.

v As

the materials are arranged in a systematic way in racks and bins, handling of

stores become very easy.

v Unnecessary

confusion and delay in issue of material avoided.

v It

helps to operate shops efficiently.

v Overstocking

is a avoided and delays due to lack of material prevented.

v Wastage

of time and labour, leakage, thefts and pilfering of stores are reduced to

their minimum.

v Classification

of receipts and issues are made easy.

v Each

item issued can be traced to its respective department, so as to ensure correct

costing.

v To safeguard the materials which are lying in store.

IMPORTANCE

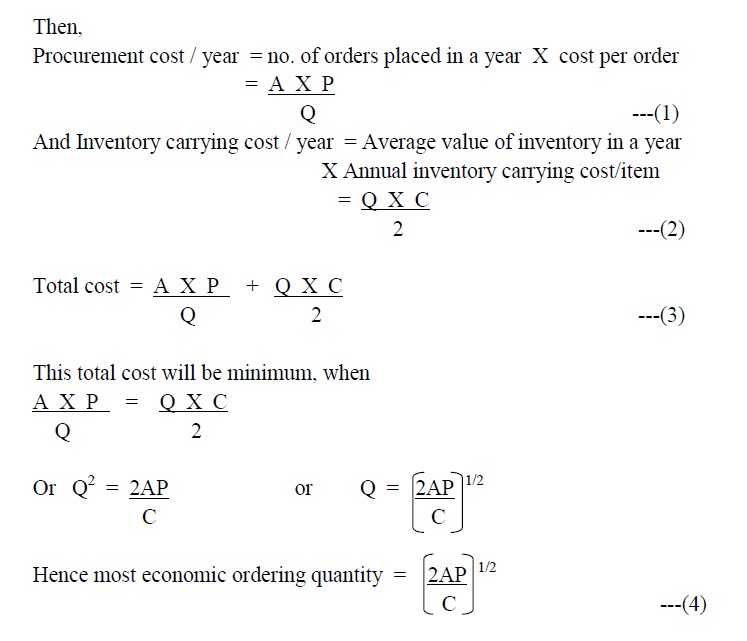

OF ECONOMIC ORDERING QUANTITY (EOQ) ANALYSIS

v The

evaluation of the most economic quantity to be purchased involves calculation

of the following two costs:

(1) Procurement

cost:- This cost includes the expenditure made on:

ð Calling

quotations.

ð Processing

quotations.

ð Placing

purchase orders.

ð Receiving

and inspecting.

ð Verifying

and payment of bills.

ð Other

incidental charges etc.

This cost nearly

comes to Rs. 100 to Rs. 200 per order.

(2) Inventory

Carrying Cost:- This consists of expenditure made for:

ð Insurance.

ð Storage

and handling.

ð Obsolescence

and depreciation.

ð Deterioration.

ð Taxes

etc.

This cost varies

nearly 10 to 20% of the product cost.

v The economic ordering quantity is obtained by

the quantity whose procurement cost is equal to inventory carrying cost.

PRINCIPLES

OF SKILLFUL PURCHSING

Following are the main

purchasing principle:

1. Right

time: this parameter is most critical one due

to the consequences of stock out in the event of part failures.to determine the

right time, information about all the element of total lead time should be

available, i.e. internal administrative lead time of converting indent into an

order, manufacturing and transportation time and inspection lead time.

2. Right

source: following are the main sources for the

procurement of spare parts:

a.

Authorised dealers or

original manufactures.

b.

Local dealers (Holding

genuine spares only).

c. By getting them manufactured.

While selecting a source of supply for spares; timely supply, reliability, price and service facilities offered should be considered.

3. Right

price: lowest acceptable price consistent with

quality, timely supply etc. should be considered.

4. Right

quality: while inviting the tenders or placing

the enquiries, quality specifications mentions tolerances should be clearly

spelled out.

5. Right

quantity:

the problem of determining the right quantity is interlinked with the

right time. The quantity will be different for each category of space such as

maintenance, overhaul, and insurance of storable spares.

6. Right

place of delivery/ Transportation: in

most of the cases, spare parts has to be supplied directly to the consuming

projects, which may be located at far distance places from headquarter. The

place of delivery should be clearly mentioned in the supply order.

7. Right procedure: right procedure to be adopted has to be formally developed for the pre-purchase, ordering, and post purchase systems. Pre-purchase system means initiating the purchase through indents requirement, planning, selection of suppliers, obtaining quotations and evaluating them. With purchase order generally an acknowledgment copy is also sent to the supplier, who then return it as a written acceptance of supply order and to abide by the terms and conditions mentioned in the order. Post purchase system include follow up with the supplies.

8. Right contract: purchase order is a legal document that binds selling company with the buying company various terms and condition about insurances, sales tax, octrai, customs, breach of contract, settlement of dispute, F.B.O., C.I.F., etc. should be clearly mentioned

DUTIES OF PURCHASE OFFICERS

v The

most important and essential duties of purchasing officer are:

ð To

maintain the standard of quality of product by selecting right quality of

materials during purchases.

ð To

organise and direct the purchasing department for efficient working.

ð To

represent his concern with other concerns during purchasing contacts.

ð He

should maintain the reputation of the concern for integrity and fair dealing

with others while negotiating.

ð Shops

should not wait for materials.

ð To

make a final check on all the requisitioned goods from different shops in the

interest of economy, as regards quality, quantity and specifications.

ð To

act as an executive of the firm and a partner, especially in the preparation of

purchasing budget.

ð To

spend money on purchases very carefully and wisely.

ð To

suggest if the materials can economically be produced in the concern instead of

purchasing and vice-versa.

Thanks for sharing the process but do you think that Cotton Tote Bag Manufacturers in India also follow the same process for managing their products and services? Because they have to deal with a lot of cotton raw material and also the quality of final tote bags should be good in order to export it to multiple countries.

ReplyDeletevery nice Info shared by you. thanks for sharing such interesting info about MM ,I am student of MBA and doing my Online MBA course in material management from

ReplyDeletedistance learning center and i have find this very informative, keep sharing.

Wow!! I am very impressed with your lovely post... I am so glad to left a comment on this...This has been a so interesting read, would love to read more here…. if anyone looking for ERP Software for SMEs (Small and Medium Enterprises)

ReplyDelete